Positioning at the intersection of late-cycle risk appetite, safe-haven distortions, and multi-timeframe currency alignment.

Global FX markets enter the final weeks of 2025 with a complex but coherent macro backdrop. Volatility remains suppressed, equity markets are resilient, and headline risk sentiment appears constructive. However, beneath the surface, several macro indicators signal underlying economic stress and late-cycle dynamics that demand selective positioning rather than broad risk exposure.

The VIX at 14.91 reflects calm surface conditions, yet the Gold–Oil ratio at 76.72 remains historically elevated, highlighting a persistent divergence between financial asset optimism and real-economy demand signals. Bond yields across developed markets remain restrictive, reinforcing yield-driven currency differentials while pressuring growth-sensitive assets.

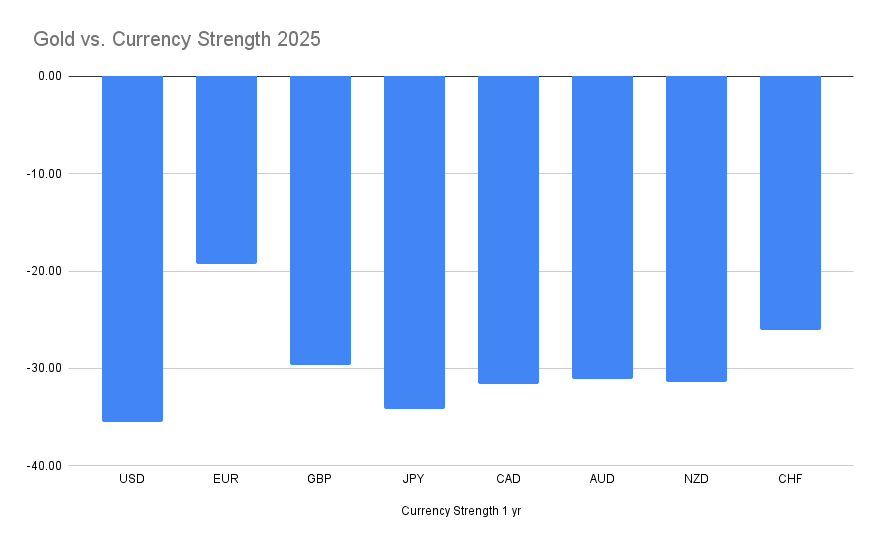

From a currency perspective, gold-denominated strength metrics continue to reveal broad currency depreciation versus gold across all major currencies on longer time horizons. Shorter-term momentum shows partial stabilization, but longer-term trends remain intact. As a result, the highest-quality FX opportunities are found not in isolated signals, but in multi-timeframe alignment, particularly in JPY crosses and selective GBP and CHF expressions.

This report synthesizes macro conditions, risk sentiment, yield structures, and gold-relative currency strength to identify high-conviction trade themes appearing across Timeline 3 and Timeline 4 only, in accordance with strict filtering rules.

Global Macro Overview

Volatility and Risk Regime

The VIX at 14.91 places markets firmly within a low-volatility regime. Historically, such conditions are associated with complacency, carry-friendly environments, and a willingness to hold directional risk. However, low volatility alone is not sufficient to confirm durable risk-on conditions. It must be evaluated alongside cross-asset stress indicators and macro ratios.

While equity markets have not yet repriced downside risk aggressively, volatility compression at this stage of the cycle increases asymmetry. Downside shocks tend to be underpriced when volatility is structurally low, making relative-value FX trades preferable to outright beta exposure.

Gold–Oil Ratio: Stress Beneath the Surface

The Gold–Oil ratio stands at 76.72, down from last week but still dramatically above historical norms of 10–30. At current levels:

- Gold is expensive relative to oil

- Oil prices reflect weak demand expectations

- Investors continue to prioritize capital preservation over growth exposure

Historically, elevated gold-to-oil ratios emerge during periods of economic stress, disinflationary impulses, or late-cycle slowdowns. While the recent pullback suggests marginal improvement, the absolute level remains incompatible with a healthy expansion.

The implication for FX markets is clear: risk appetite is selective and fragile, favoring currencies with yield support or structural defensiveness rather than broad pro-cyclical exposure.

Rates, Yields, and Monetary Differentials

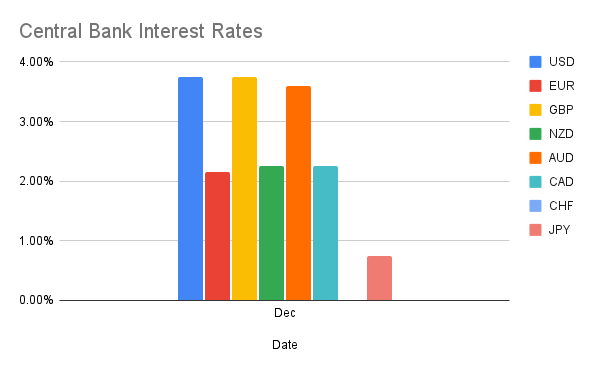

Central Bank Policy Snapshot

Interest-rate differentials remain a dominant FX driver:

- USD: 3.75%

- GBP: 3.75%

- AUD: 3.60%

- CAD: 2.25%

- EUR: 2.15%

- JPY: 0.75%

- CHF: Lowest among majors

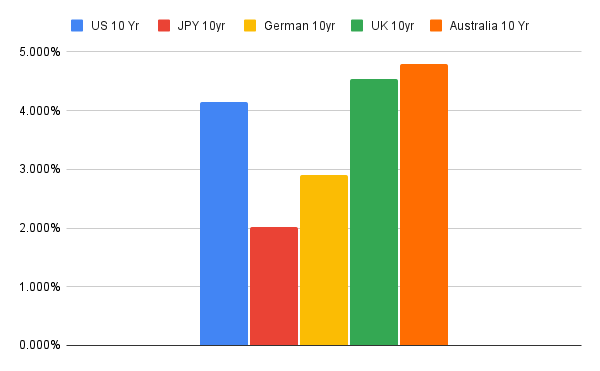

10-Year Government Bond Yields

Long-term yields reinforce this divergence:

- Australia: 4.798% (highest)

- UK: 4.535%

- United States: 4.149%

- Germany: 2.907%

- Japan: 2.018%

Elevated long-term yields imply sustained financial tightness and place downward pressure on growth-sensitive sectors. For FX, this environment favors yield-backed currencies over structurally low-yielding funding currencies, particularly when confirmed by multi-timeframe strength analysis.

Safe-Haven vs Risk Dynamics

Despite the working assumption of a “risk-on” environment due to equity resilience and suppressed volatility, safe-haven demand has not fully unwound. This is evident in:

- Persistent gold outperformance versus currencies on a 1-year basis

- Weak oil pricing relative to gold

This hybrid regime—risk-on at the surface, defensive beneath—typically produces relative-strength FX opportunities rather than uniform directional trends. Traders should therefore prioritize currency-against-currency imbalances where macro, yield, and strength metrics align.

Currency Breakdown (Macro + Gold-Relative Context)

USD

- S&P 500 vs Gold: 1.58

- 10-year yield: 4.149%

- Policy rate: 3.75%

The USD benefits from yield support and equity resilience, yet remains structurally weak versus gold on longer horizons. This suggests USD strength is tactical rather than secular, favoring selective USD shorts against stronger currencies or safe havens rather than blanket USD selling.

EUR

- DAX vs Gold: 6.56 (average)

- CAC 40 vs Gold: 2.20 (below historical mean of 4–5)

- 10-year Bund: 2.907%

- Policy rate: 2.15%

The euro remains a middle-of-the-pack currency, lacking yield dominance and exhibiting equity underperformance versus gold in parts of the region. EUR is best traded relatively, particularly against structurally weaker or lower-yielding counterparts.

GBP

- FTSE 100 vs Gold: 3.05

- 10-year yield: 4.535%

- Policy rate: 3.75%

Sterling remains one of the more complex currencies in the G10. Yield support is strong, but equity performance versus gold is unimpressive. This divergence creates excellent relative-value opportunities, especially in GBP crosses rather than outright GBP exposure.

JPY

- Nikkei 225 vs Gold: 0.072 (lower end of normal range)

- 10-year JGB: 2.018%

- Policy rate: 0.75%

JPY remains the primary funding currency. Ultra-low yields and weak equity performance relative to gold reinforce its vulnerability in risk-stable environments. As long as volatility remains contained, JPY shorts against higher-yielding currencies remain structurally favored.

AUD

- 10-year yield: 4.798% (highest among peers)

- Policy rate: 3.60%

AUD continues to benefit from yield appeal but remains sensitive to global growth and commodity demand. Gold-relative weakness tempers enthusiasm, making AUD best suited as a carry expression against JPY rather than as a broad risk proxy.

CAD

- Policy rate: 2.25%

CAD lacks yield dominance and is exposed to weak oil dynamics. With oil underperforming gold, CAD strength is structurally constrained, particularly against currencies benefiting from carry or safe-haven demand.

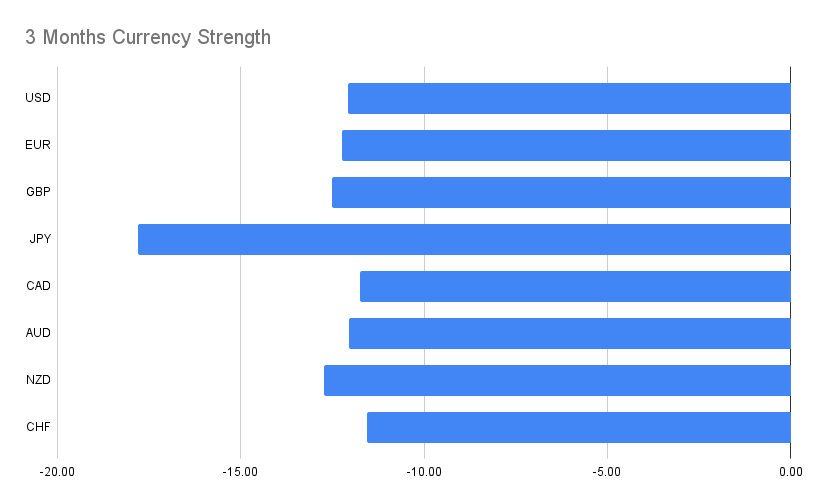

Gold-Relative Currency Strength (Multi-Timeframe Perspective)

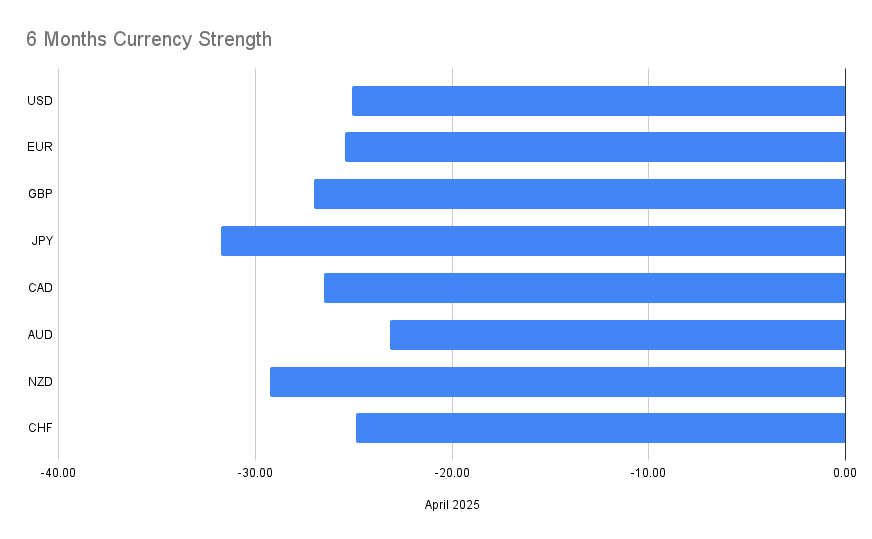

Across 1-year, 6-month, 3-month, and December-only horizons, all major currencies remain negative versus gold on longer timeframes. This reinforces gold’s role as the ultimate benchmark and underscores the importance of relative FX positioning.

Shorter-term charts show some compression in losses, but no decisive trend reversal. As a result, the highest-quality trades are those that appear consistently across multiple horizons, indicating persistent structural forces rather than short-term noise.

Recommended Trades (Timeline 3 & 4 Only)

Trades Appearing in ALL 4 Time Frames

Highest-conviction, structurally aligned positions

| Pair | Direction | Rationale |

|---|---|---|

| USDCHF | SELL | Yield convergence + CHF defensive strength |

| EURJPY | BUY | Euro stability vs persistent JPY funding weakness |

| EURNZD | BUY | Structural NZD weakness vs EUR |

| GBPJPY | BUY | Yield differential + JPY funding dynamics |

| GBPCAD | SELL | Oil weakness + CAD underperformance |

| GBPNZD | BUY | GBP yield support vs NZD weakness |

| GBPCHF | SELL | CHF safe-haven resilience |

| CADJPY | BUY | Carry structure favors CAD over JPY |

| AUDJPY | BUY | Strong yield differential |

| NZDJPY | BUY | Carry trade alignment |

| CHFJPY | BUY | CHF stability vs JPY weakness |

These trades exhibit complete alignment from short-term (December) through long-term (1-year), making them suitable for:

- Core swing positions

- Position-trading frameworks

- Multi-horizon portfolio anchors

Trades Appearing in Exactly 3 Time Frames

| Pair | Direction | Rationale |

|---|---|---|

| USDCAD | SELL | USD tactical strength fading vs CAD stabilization |

| EURGBP | BUY | Relative EUR resilience vs GBP mean-reversion |

Market Risks & Forward Guidance

Key risks to monitor going forward include:

- A volatility regime shift that disrupts carry structures

- Further deterioration in oil demand signaling sharper growth slowdown

- Policy communication shifts from central banks affecting yield spreads

.

Conclusion

The December 21st macro landscape is defined by surface-level calm masking deeper structural tensions. Low volatility and resilient equities coexist with elevated gold ratios, restrictive yields, and broad currency weakness versus gold. In such an environment, success in FX does not come from chasing risk, but from aligning with persistent, multi-timeframe relative-strength themes.