War, Inflation, and the Fragile Carry Trade

By Takezo Trading | 14 March 2026

The global macro environment continues to shift as geopolitical tensions escalate and markets attempt to price the consequences of war, inflation, and tightening liquidity. The developing conflict between the United States and Iran has introduced new uncertainty into global supply chains, commodity markets, and risk sentiment.

Energy markets are reacting, gold continues consolidating near elevated levels, and volatility has re-entered the market. Meanwhile, currency traders face a week loaded with central bank decisions across the major economies.

This report breaks down the macro drivers shaping the FX market and outlines the highest-probability trade setups based on cross-asset signals and multi-timeframe analysis.

Estimated reading time: 8 minutes

This Week’s Bottom Line

Several powerful macro forces are converging at once.

First, geopolitical risk has intensified as the conflict between the United States and Iran continues to disrupt trade flows and energy markets. Oil prices are rising, and the strategic Strait of Hormuz — one of the world’s most important energy chokepoints — faces disruption. This creates an environment where inflationary pressures can rapidly return to global markets.

Second, gold remains elevated as countries gradually diversify away from U.S. Treasury holdings and increase gold reserves. Large economies such as China and Japan continue shifting parts of their reserve strategies toward physical gold as a hedge against geopolitical risk and monetary uncertainty.

Third, volatility is beginning to return to markets. The VIX index is approaching the $30 level, signaling rising demand for hedging and protection. Historically, sustained moves toward this range signal increasing uncertainty across risk assets.

The result is a market regime defined by risk-on behavior mixed with underlying caution. Carry trades remain active, but the macro backdrop is increasingly fragile.

Market Regime: Risk-On, But Fragile

Despite rising geopolitical tension, global investors have not yet fully retreated from risk assets.

Japanese carry trades remain active, supported by relatively low interest rates in Japan compared with higher yields in the United States, Australia, and the United Kingdom. As long as global liquidity remains sufficient and volatility stays contained, these carry trades can continue supporting risk currencies.

However, several warning signals suggest the current regime could shift quickly:

- Gold remains elevated

- Oil prices are rising

- Volatility is approaching stress levels

- Supply chains face disruption due to war

If inflation expectations begin accelerating again, central banks could be forced to maintain restrictive monetary policies longer than markets currently expect.

This tension between carry trade optimism and macro uncertainty is likely to define FX markets in the coming weeks.

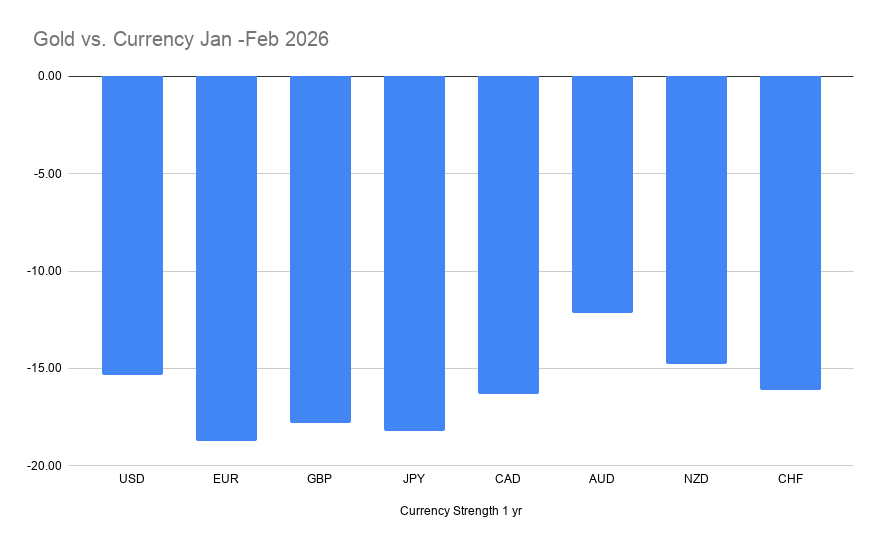

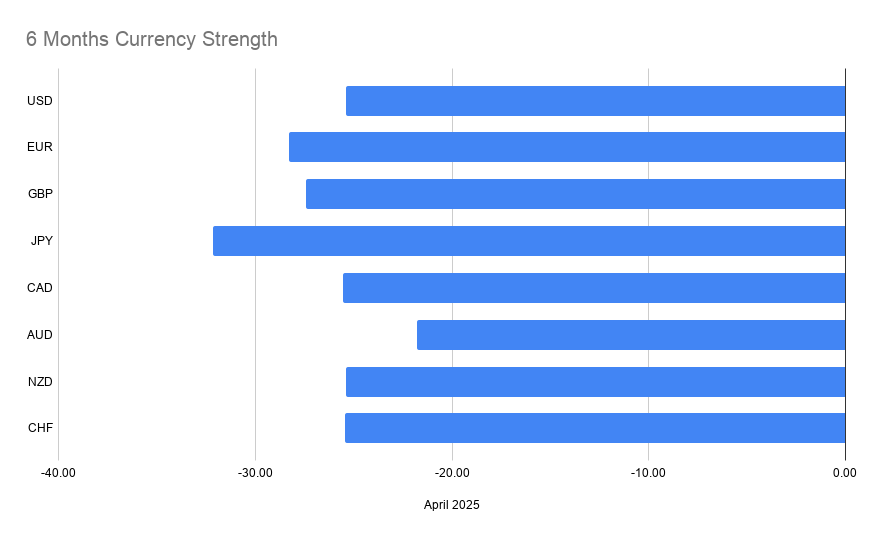

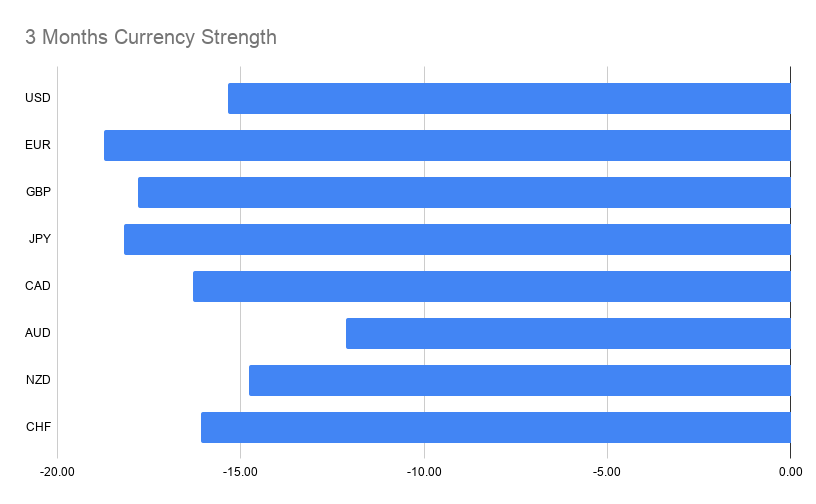

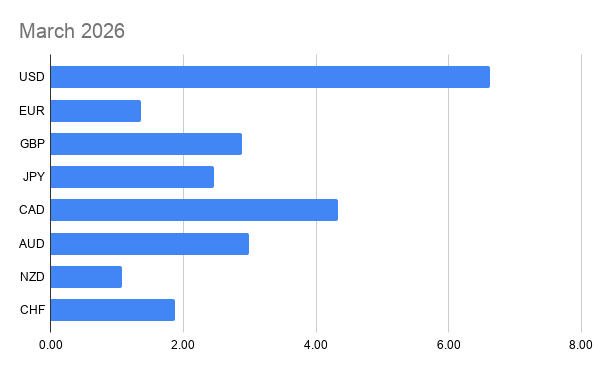

FX Watchlist — Currency strength as measured against Gold; Multi-Timeframe Trade Alignment

Trade Setups Appearing in All 4 Timeframes

(Same pair and same direction in March, 3M, 6M, and 2026)

EURUSD – SELL

GBPUSD – SELL

USDJPY – BUY

USDCAD – BUY

USDCHF – BUY

EURGBP – SELL

EURCAD – SELL

EURAUD – SELL

GBPJPY – BUY

GBPCAD – SELL

GBPAUD – SELL

CADJPY – BUY

AUDNZD – BUY

AUDCHF – BUY

Trade Setups Appearing in Exactly 3 Timeframes

AUDUSD – BUY

EURJPY – SELL

NZDJPY – BUY

CHFJPY – BUY

AUDCAD – BUY

NZDCAD – BUY

CADCHF – SELL

NZDCHF – SELL

Market Snapshot — What Happened Last Week

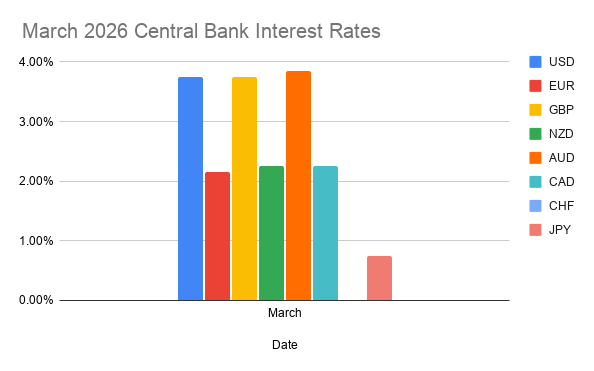

Interest Rates

Central bank policy remains the dominant driver of currency valuations. Current policy rates across major economies show meaningful divergence:

| Currency | Policy Rate |

|---|---|

| USD | 3.75% |

| EUR | 2.15% |

| GBP | 3.75% |

| NZD | 2.25% |

| AUD | 3.85% |

| CAD | 2.25% |

| CHF | 0% |

| JPY | 0.75% |

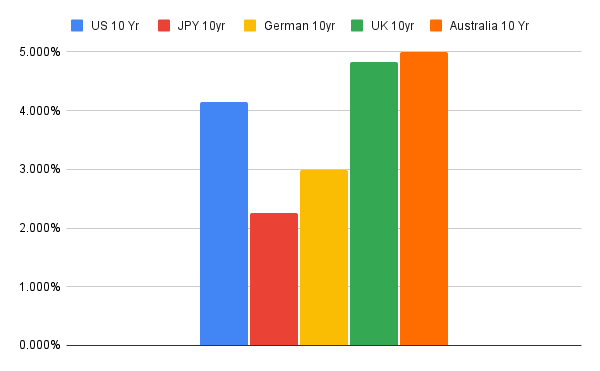

Global Bond Yields

Long-term yields remain elevated in several developed economies.

| Country | 10-Year Yield |

|---|---|

| United States | 4.283% |

| Japan | 2.248% |

| Euro Area | 2.987% |

| United Kingdom | 4.836% |

| Australia | 4.996% |

Higher yields typically attract capital inflows, strengthening currencies associated with stronger return opportunities.

Equity vs Gold Ratios

Comparing stock markets to gold offers insight into global risk sentiment.

| Market | Equity / Gold Ratio |

|---|---|

| S&P 500 | 1.32 |

| DAX | 5.33 |

| CAC40 | 1.80 |

| FTSE 100 | 2.70 |

| Nikkei 225 | 0.068 |

Volatility

The VIX index currently sits at $27.19, approaching levels associated with growing market stress.

Commodities

One important macro signal remains the Gold-to-Oil Ratio, currently sitting at 50.63.

This ratio helps traders understand the relationship between safe-haven demand (gold) and economic activity or inflation pressure (oil).

When both gold and oil are rising simultaneously, it often reflects stagflationary risk, where inflation pressures rise even as growth uncertainty increases.

Central Bank Event Risk This Week

The upcoming week contains a cluster of major central bank decisions, creating one of the most important macro calendars of the quarter.

High-Impact Events

Australian Cash Rate Decision — March 17

Markets currently price the possibility of a rate increase toward 4.10% from 3.85%.

- A hike would likely strengthen the Australian dollar.

- A pause or cut would be bearish for AUD.

Bank of Canada Rate Decision — March 18

Markets expect no rate change.

However, oil prices are rising due to geopolitical tensions. If inflation risks accelerate, the Bank of Canada may need to maintain tighter policy.

- Rate hike or hold = bullish CAD

- Rate cut = bearish CAD

Federal Reserve Decision — March 18

Markets expect the Fed to hold rates steady.

Given rising oil prices and global geopolitical risk, any hint that inflation remains persistent could support the U.S. dollar.

Bank of Japan Policy Decision — March 19

Markets expect no rate change.

However, any move toward tighter policy would likely produce a sharp rally in the yen.

Swiss National Bank Decision — March 19

Rates are expected to remain at 0%.

Any unexpected tightening would strengthen the Swiss franc significantly.

Bank of England Decision — March 19

Markets expect the Bank Rate to remain at 3.75%.

- Rate cut → bearish GBP

- Rate hike → bullish GBP

European Central Bank Decision — March 19

Markets expect the ECB to hold rates at 2.15%.

The euro will likely react strongly if policymakers hint at either renewed tightening or earlier easing.

Key Event Risk Days

The most important trading days this week will likely be:

March 17–19

This window contains the majority of global central bank decisions and has the potential to reshape currency market expectations.

Final Thoughts

Global markets are entering a period where geopolitics, inflation, and monetary policy are colliding simultaneously.

Oil prices are rising, gold remains elevated, and volatility is climbing. Yet carry trades continue operating beneath the surface.

This creates a fragile equilibrium — one that can persist temporarily but may break suddenly if macro conditions shift.

For traders, the focus should remain on multi-timeframe alignment and disciplined risk management.

If geopolitical tensions escalate and oil continues rising, inflation could return as the dominant market narrative.

If that happens, currency markets may quickly transition into a much more volatile regime.