A risk-on regime remains intact, but rising Japanese yields and persistent gold strength are early warning signals that carry-driven positioning could unwind quickly if policy or geopolitics disrupts the current calm.

Week Ending: 16 Jan 2026

By: Takezo Trading

Estimated Reading Time: 6–8 minutes

Executive Summary

This Week’s Bottom Line

- Macro driver: Japan is the fulcrum. Rising JGB yields are the key stress point for global carry and risk appetite.

- Market regime: Risk-on, but fragile. Volatility is low, yet “insurance” demand (gold) remains persistent.

- Primary risks to monitor:

- Japan’s 10Y yields are rising. Carry still works for now as Japan’s 10yr Bond rates rises, but a continuation higher can accelerate de-risking and force a disorderly unwind.

- Gold is outperforming fiat currencies. Gold is blowing out fiat currency, this is a key indicator of flight to safety, but other signals don’t show this, hence I still think we are in a risk on atmosphere. Gold is high and growing as countries try to decouple from the USD, and trading in their treasury bonds for Gold, for example, China and Japan.

- Geopolitics and supply chain risk remain a background accelerant; escalation can flip sentiment rapidly and reprice FX through safe-haven flows.

Bias Map

- Pro-risk / anti-risk: Pro-risk bias, with conditional risk controls (watch Japan + geopolitical catalysts closely).

- Core framework this week: If Japan tightens (or markets believe it will), carry unwinds → risk-off → JPY strength and broader deleveraging risk.

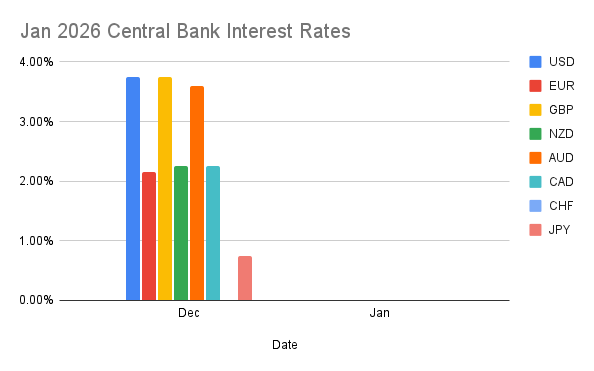

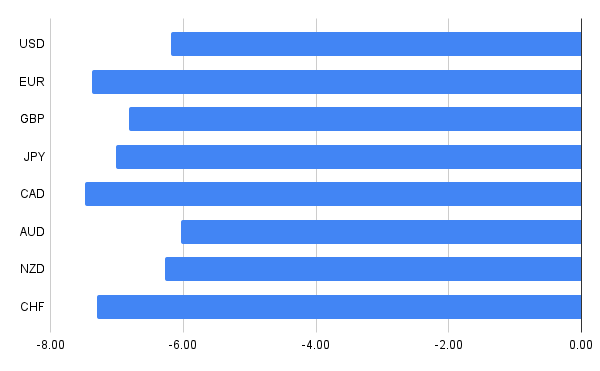

Central Bank Rates (Policy Backdrop)

| Currency | Policy Rate |

|---|---|

| USD | 3.75% |

| EUR | 2.15% |

| GBP | 3.75% |

| NZD | 2.25% |

| AUD | 3.60% |

| CAD | 2.25% |

| CHF | 0.00% |

| JPY | 0.75% |

Interpretation:

- Rate differentials still support carry, particularly against low-yield funding currencies.

- However, Japan is no longer “static.” When JPY funding becomes less reliable, leverage often exits across multiple asset classes—not only FX.

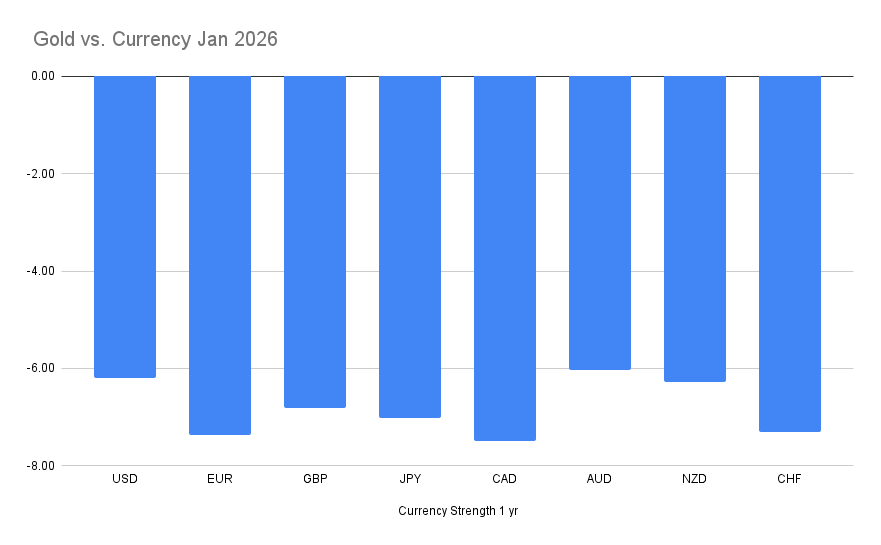

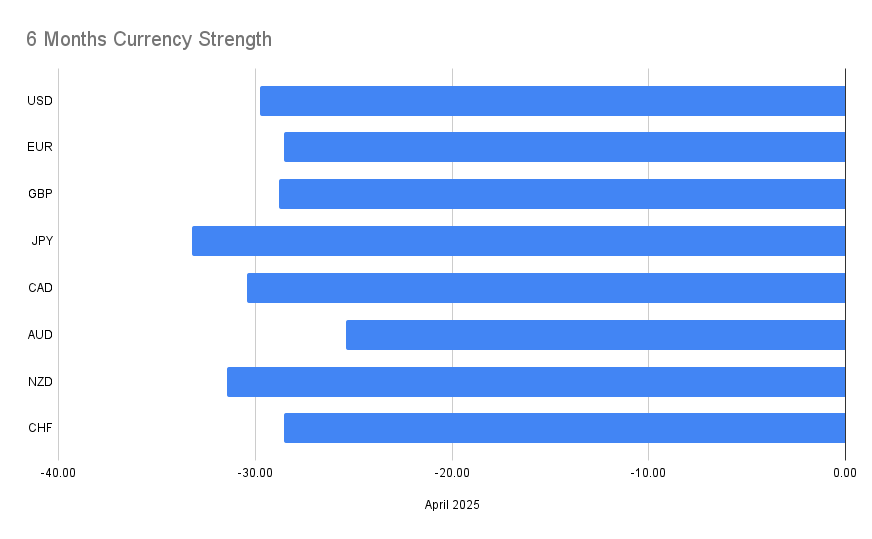

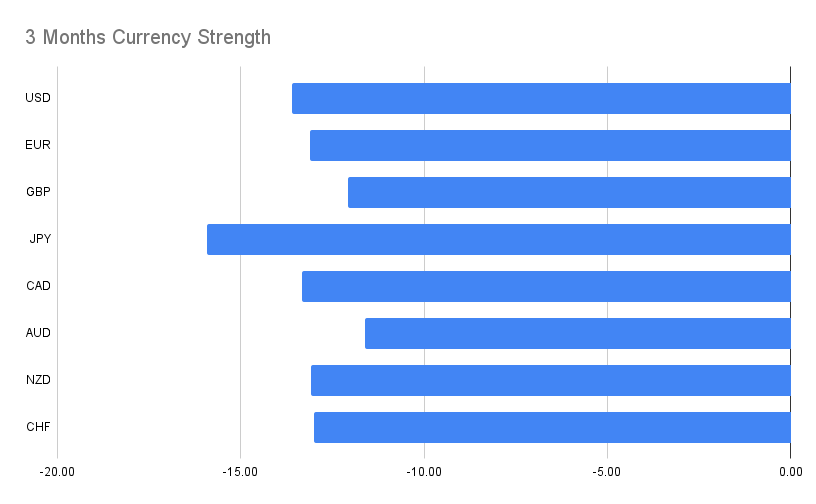

FX Watchlist (Based on Gold vs. Each Currency)

USDJPY — BUY

AUDUSD — BUY

EURCAD — BUY

EURAUD — SELL

GBPJPY — BUY

GBPCAD — BUY

GBPAUD — SELL

AUDJPY — BUY

NZDJPY — BUY

AUDCAD — BUY

AUDNZD — BUY

AUDCHF — BUY

How to read this list:

This watchlist is derived from a gold-relative framework—identifying which currencies are weakening the most against gold and translating that into FX opportunity. The goal is to keep the process systematic while still respecting the macro regime risks (especially Japan).

Market Snapshot (What Happened Last Week)

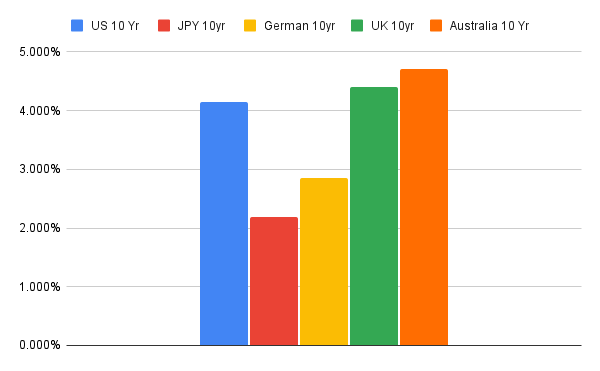

1) Rates: 10Y Government Bond Yields

- US 10Y: 4.227%

- Germany 10Y: 2.847%

- UK 10Y: 4.403%

- Japan 10Y: 2.184%

- Australia 10Y: 4.708%

What it suggests:

Japan stands out. A 10Y yield move in Japan is not “just local”—it can change global financing conditions because JPY funding is a foundational pillar of carry and leverage.

2) Equities vs Gold Ratios

- S&P 500 vs Gold: 1.51

- DAX vs Gold: 6.38

- CAC 40 vs Gold: 2.08

- FTSE 100 vs Gold: 2.98

- Nikkei 225 vs Gold: 0.073

Interpretation:

Equity performance looks stable on the surface, but gold’s relative strength suggests a segment of global capital is still hedging policy and geopolitical tail risk.

3) Volatility (VIX): 15.86

Interpretation:

Low volatility supports risk-on positioning—until it doesn’t. VIX at these levels can encourage complacency and crowded positioning.

4) Commodities: Gold/Oil Ratio — 77.58

Interpretation:

A higher gold/oil ratio can align with either (a) stronger demand for monetary hedges, or (b) softer growth impulses relative to inflation hedging. Context matters, but the message is clear: gold is still being treated as strategic protection.

Data Calendar & Event Risk (The Watch List)

High-impact events (what can change the regime)

| Event | Timing | Why it matters | What would move FX |

|---|---|---|---|

| President Trump Speaks | Wed 21st, 9am | Potential for sudden geopolitical / trade / policy messaging | Surprise tone or policy hints can trigger USD moves and risk sentiment repricing |

| Australia Employment Data | Wed 21st | Near-term AUD volatility catalyst | Large deviation from expectations can move AUD short-term, but may not set the long-term trend alone |

| Bank of Japan Policy Rate | This week | Highest-leverage regime risk: BOJ tightening threatens carry | Any signal of tighter policy (or willingness to tolerate higher yields) can strengthen JPY and spark broad de-risking |

The key takeaway:

This week is not about how many events are on the calendar. It’s about which event can break the current regime. BOJ risk is the highest leverage point.

Conclusion

If Japan’s yield rise stabilizes and risk appetite remains intact, favor the pro-risk watchlist themes. If Japan’s yields continue to rise or BOJ messaging turns more hawkish, lets see how the market reacts as it relates to the carry trades.

Trade Journal Note

Markets still reward carry and risk exposure—but only while funding is stable. Rising Japanese yields are the kind of quiet shift that can change everything without warning. This week, discipline means staying systematic while respecting the one variable that can flip the board: Japan.

Key Definition

Carry trade (simple definition): Borrow in a low-yielding currency (often JPY or CHF) and invest in higher-yielding assets/currencies to capture the interest-rate differential. This works best when volatility is low and funding costs are stable.

Further Reading

If you want deeper context on macro stress signals, here is a practical guide you can use alongside this weekly outlook:

Gold/Oil Ratio Guide:

https://takezotrading.com/the-gold-to-oil-ratio-a-historical-and-practical-guide/