A concise assessment of the dominant macro forces shaping currency markets, cross-asset risk sentiment, and actionable FX positioning for the week ahead.

Takezo Trading | 14 Feb 2026

Macro Backdrop

Global foreign-exchange markets remain anchored in a pro-risk but fragile regime, where supportive liquidity and carry dynamics coexist with rising geopolitical and structural uncertainty.

Key macro drivers currently in focus include:

- Japanese bond yields trending higher, posing latent risk to the global carry trade complex should tightening financial conditions accelerate.

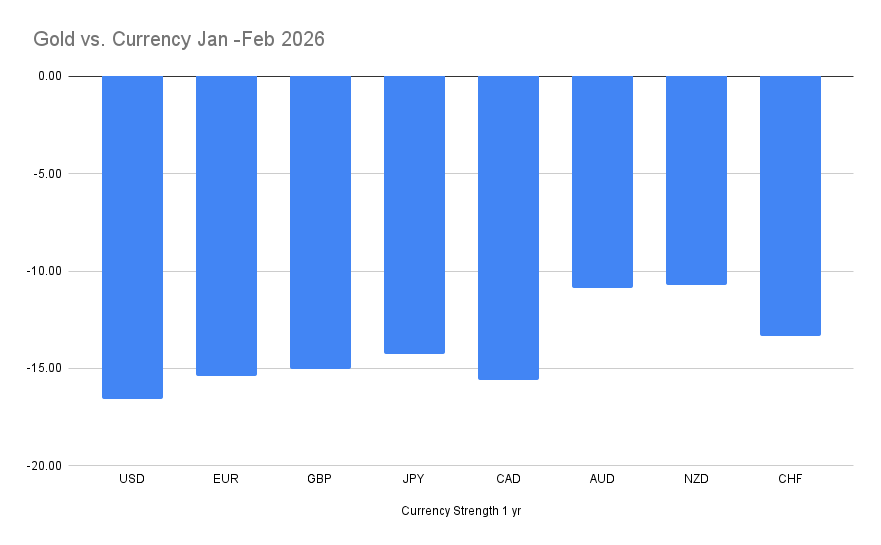

- Persistent strength in gold relative to fiat currencies, signaling underlying reserve diversification and latent safe-haven demand despite broadly risk-on market behavior.

- Escalating geopolitical tensions involving Iran, which introduce tail-risk scenarios capable of rapidly shifting global risk sentiment and capital flows.

Together, these forces define a market environment where risk appetite persists, yet conviction remains conditional.

Regime Assessment

- Market tone: Constructive risk sentiment, though increasingly cautious.

- Structural tension: Safe-haven signals (gold strength) diverge from equity resilience and moderate volatility.

- Strategic implication: FX positioning should balance carry exposure with downside hedging discipline.

Bias Map

Risk Orientation:

Overall bias remains pro-risk, supported by ongoing carry trade dynamics and stable growth expectations. However, geopolitical escalation or disorderly bond-market repricing could quickly reverse this stance.

FX Framework:

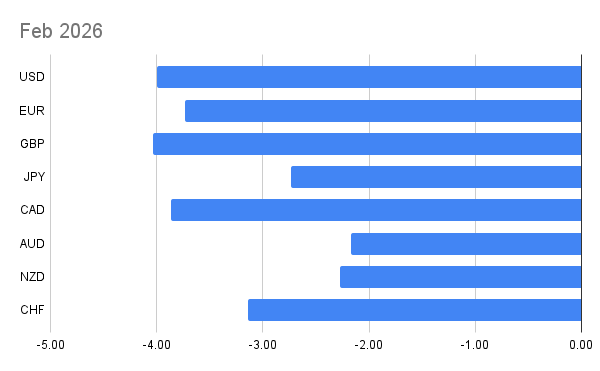

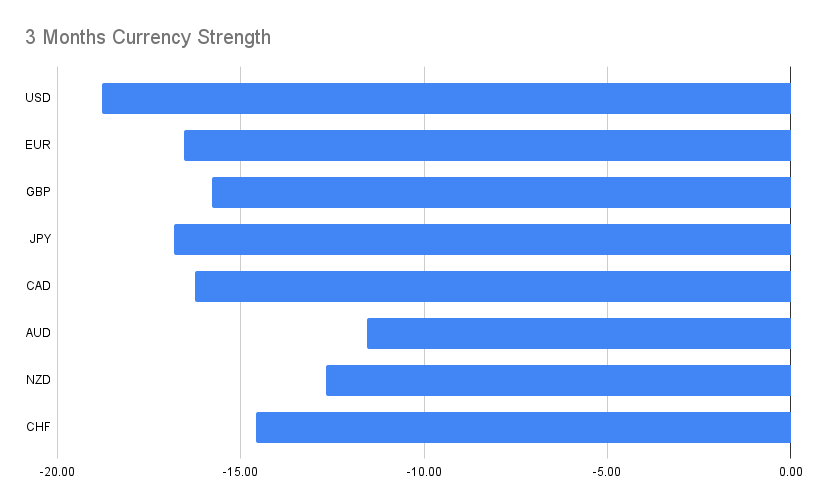

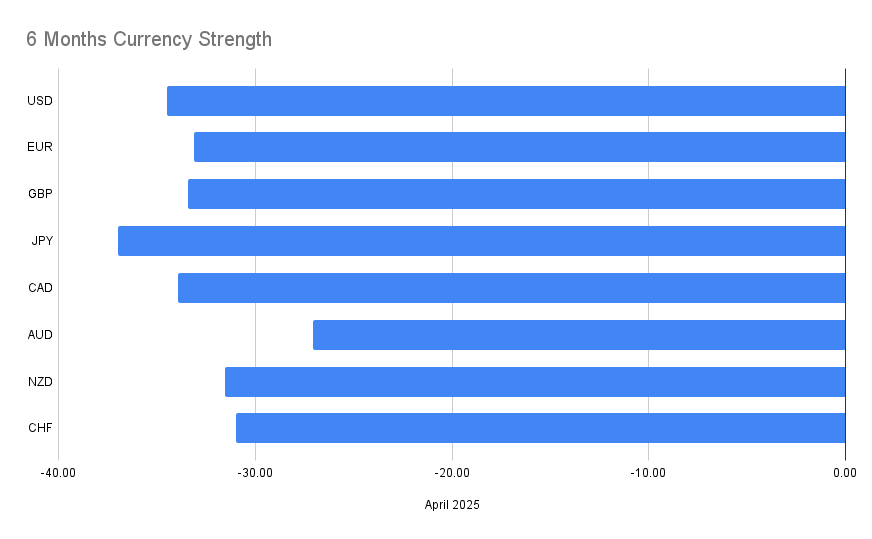

Primary directional signals continue to derive from Gold-versus-Currency alignment across multiple time horizons, which remains the most internally consistent cross-asset indicator.

Multi-Timeframe FX vs Gold Setups:

3 Timeframes confluence

GBPUSD- BUY

USDJPY- SELL

EURCAD- BUY

GBPCAD- BUY

CHFJPY- BUY

AUDNZD- BUY

NZDCHF- BUY

All 4 Timeframes Confluence

EURUSD- BUY

USDCAD- SELL

AUDUSD- BUY

NZDUSD- BUY

USDCHF- SELL

EURAUD- SELL

EURNZD- SELL

EURCHF- SELL

GBPAUD- SELL

GBPNZD- SELL

GBPCHF- SELL

AUDJPY- BUY

NZDJPY- BUY

AUDCAD- BUY

NZDCAD- BUY

CADCHF- SELL

AUDCHF- BUY

Market Snapshot — What Happened Last Week

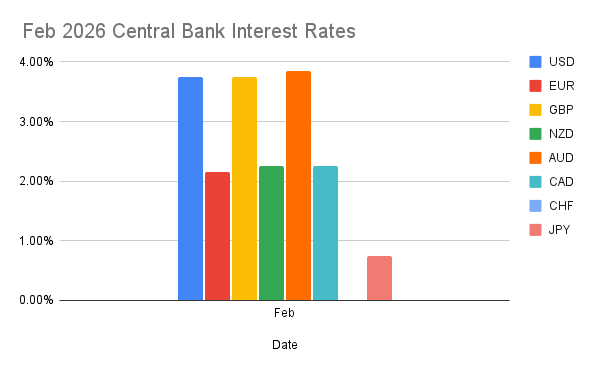

Global Interest Rates

Policy settings remain uneven across developed economies:

- USD: 3.75%

- EUR: 2.15%

- GBP: 3.75%

- AUD: 3.85%

- NZD: 2.25%

- CAD: 2.25%

- JPY: 0.75%

- CHF: 0%

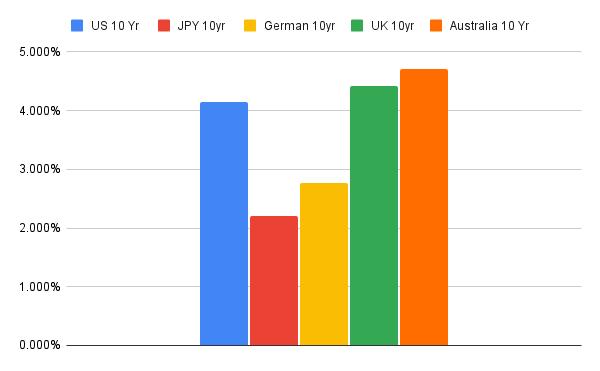

10-Year Sovereign Yields

- United States: 4.05%

- United Kingdom: 4.42%

- Australia: 4.71%

- Euro Area: 2.76%

- Japan: 2.21%

The notable development is Japan’s rising long-term yield structure—an early warning signal for potential global carry compression.

Equities vs Gold Ratios

Cross-asset valuation signals remain mixed:

- S&P 500 / Gold: 1.36

- DAX / Gold: 5.87

- CAC 40 / Gold: 1.96

- FTSE 100 / Gold: 2.83

- Nikkei 225 / Gold: 0.074

Gold’s relative resilience continues to contradict pure risk-on narratives.

Volatility

- VIX: 20.6

Volatility has risen meaningfully but remains below systemic stress thresholds (~30), reinforcing the cautious-risk regime.

Commodities

- Gold-to-Oil Ratio: 80.3

- https://takezotrading.com/the-gold-to-oil-ratio-a-historical-and-practical-guide/

Data Calendar & Event Risk

Tier-1 Catalysts

Reserve Bank of New Zealand Policy Decision — 17 Feb

- Market expectation: Rates unchanged.

- Bullish NZD scenario: Hold or hike.

- Bearish scenario: Unexpected dovish shift.

US Initial Jobless Claims

- Consensus: ~229k vs prior 227k.

- Higher claims: USD negative.

- Lower claims: USD supportive.

Commitment of Traders Positioning