War, Gold, and Rising Oil: The Macro Forces Reshaping Currency Markets

By Takezo Trading | 07 March 2026

Estimated Reading Time: 10–12 minutes

Executive Summary — The Battlefield This Week

Currency markets are entering a period where geopolitics, commodities, and monetary policy are colliding in ways that traders cannot ignore. The macro environment has shifted from a relatively stable cycle into one dominated by war risk, inflation pressures, and safe-haven demand.

Several signals across markets point toward a regime that is simultaneously risk-seeking and defensive, a paradox that often appears during the early stages of major geopolitical conflict.

This Week’s Bottom Line

- Primary Macro Driver: Geopolitical escalation following the outbreak of war between the United States and Iran.

- Market Regime: Risk-on but cautious — long-term inflation expectations rising while short-term flows move toward safety.

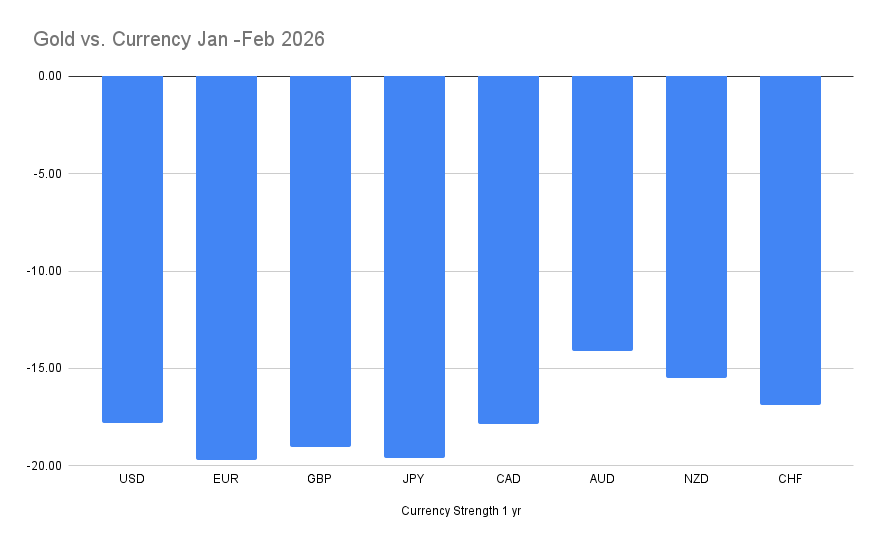

- Gold vs Fiat: Gold continues to outperform global currencies, signaling capital seeking protection outside traditional fiat systems.

- Energy Shock Risk: Oil prices are rising sharply as the Strait of Hormuz faces disruption.

- Systemic Tension: Markets are adjusting to supply chain disruptions and the potential for a wider regional conflict.

In short: the macro chessboard has changed. Traders must now watch the interaction between commodities, central banks, and geopolitics rather than focusing solely on economic data.

Understanding the Current Market Regime

In calm markets, currencies usually move according to familiar forces:

- Interest rate differentials

- Growth expectations

- Risk sentiment

But during geopolitical shocks, capital flows behave differently.

War tends to produce two distinct phases:

Phase 1 — Flight to Safety

Investors rush toward perceived safe assets:

- Gold

- US Dollar

- Japanese Yen

- Swiss Franc

This phase is driven by fear and uncertainty.

Phase 2 — Inflation and Supply Shock

Once markets begin to price the consequences of conflict, the focus shifts toward:

- Energy supply disruptions

- Fiscal spending

- Inflation expectations

Historically, wars tend to be inflationary in the long run because governments increase spending and supply chains become constrained.

The current environment suggests we are transitioning between these phases.

Gold prices remain elevated while oil is rising — a combination that usually signals both fear and inflation simultaneously.

The Gold Signal: Capital Leaving Fiat

One of the most important signals in global macro today is the continued strength of gold relative to currencies.

Gold’s strength is not just about inflation. It reflects something deeper:

A structural shift in how countries store value.

Several countries are actively increasing their gold reserves while reducing exposure to US Treasury bonds. Major economies such as China and Japan have been increasing gold holdings, reflecting a strategic effort to diversify reserve assets.

For currency traders, this matters enormously.

When gold consistently outperforms fiat currencies, it often indicates:

- Loss of confidence in monetary stability

- Increased geopolitical tension

- A transition toward defensive asset allocation

Geopolitics: The War That Could Reshape Markets

The outbreak of war between the United States and Iran has introduced a new macro risk that markets must now price.

One of the most critical developments is the disruption around the Strait of Hormuz, one of the most strategically important energy chokepoints in the world.

Roughly 20% of global oil supply passes through this corridor.

If shipping through the strait is restricted or closed, the consequences would ripple across global markets:

Immediate Impacts

- Oil price spikes

- Shipping disruptions

- Rising inflation expectations

Medium-Term Impacts

- Increased government spending

- Commodity shortages

- Currency volatility

Long-Term Impacts

- Realignment of trade networks

- Structural inflation pressures

From a macro perspective, this type of conflict tends to favor:

- Commodity currencies in the short term

- Safe-haven currencies during volatility spikes

- Countries with strong energy independence

But the effects are rarely simple.

Higher oil prices can strengthen some currencies while weakening others, depending on whether the country is a net exporter or importer of energy.

The Risk Sentiment Paradox

Markets are currently showing a mixed signal environment.

Pro-Risk Forces

Several factors are supporting risk assets:

- The Japanese carry trade remains attractive due to low Japanese interest rates.

- Global liquidity has not tightened significantly yet.

- Equity markets have not collapsed despite geopolitical tensions.

Carry trades allow investors to borrow in low-yield currencies like the yen and invest in higher-yielding assets.

This creates upward pressure on pairs such as:

- AUDJPY

- NZDJPY

- GBPJPY

Anti-Risk Signals

At the same time, several indicators suggest caution:

- Gold prices remain extremely high

- The VIX volatility index is near 30, signaling market stress

- The Middle East conflict could expand into a wider regional war

This duality explains why markets appear both optimistic and defensive at the same time.

FX Watchlist — The Highest Conviction Setups

One of the most powerful tools in macro trading is multi-timeframe alignment.

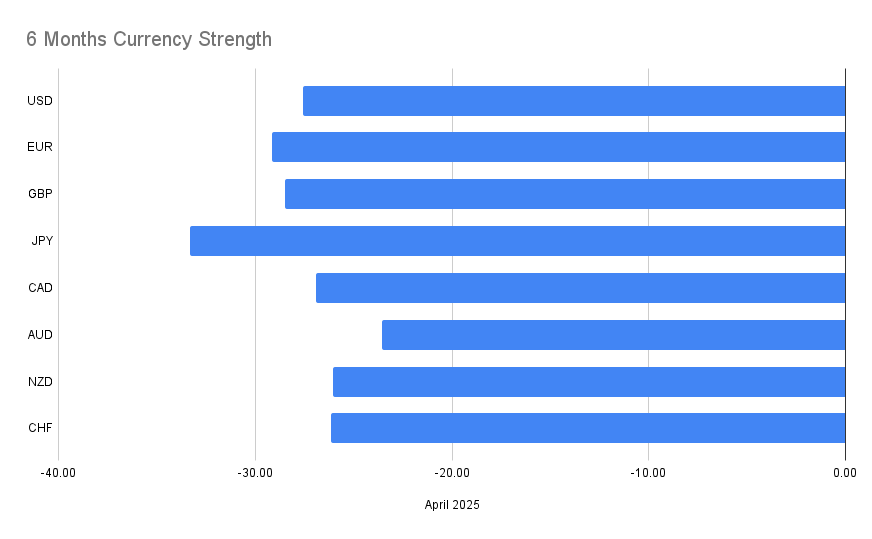

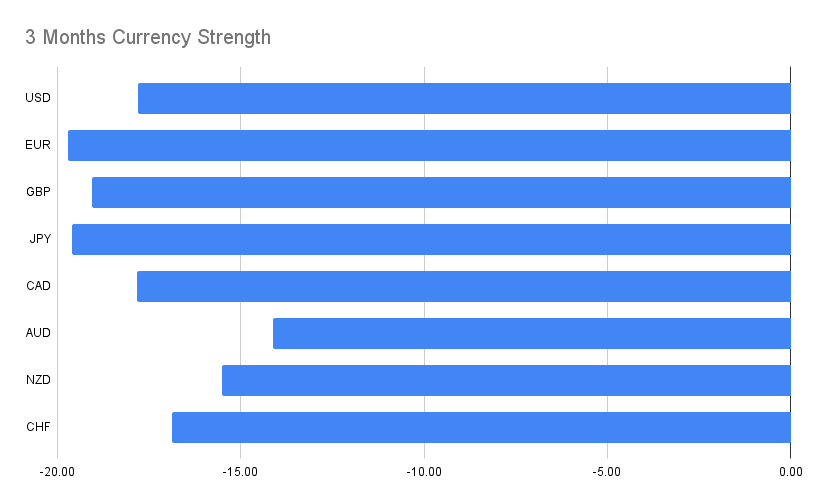

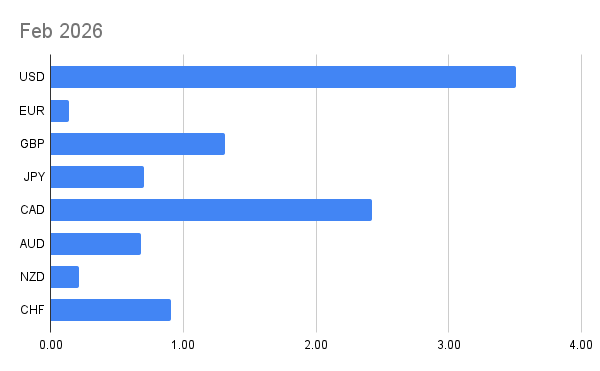

The following setups based on currency relative strength against Gold towards each other, appeared in the same direction across three major timelines:

Trades Appearing on Three Timeframes

- USDCAD — BUY

- EURJPY — SELL

- AUDJPY — BUY

- NZDJPY — BUY

- CADCHF — SELL

.

Trades Appearing on All Four Timeframes

The following pairs show complete alignment across March, 3-month, 6-month, and 2026 so far.

These tend to represent the highest conviction macro themes.

- EURUSD — SELL

- GBPUSD — SELL

- USDJPY — BUY

- EURGBP — SELL

- EURCAD — SELL

- EURAUD — SELL

- EURNZD — SELL

- EURCHF — SELL

- GBPJPY — BUY

- GBPCAD — SELL

- CADJPY — BUY

- AUDNZD — BUY

The dominant theme here is clear:

Euro weakness

Market Snapshot — Cross Asset Signals

Understanding currencies requires watching the entire macro ecosystem.

Currencies rarely move in isolation.

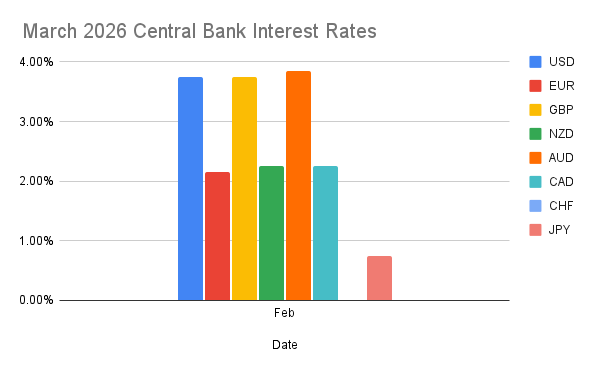

Central Bank Rates

Interest rates remain one of the most powerful drivers of capital flows.

| Currency | Rate |

|---|---|

| USD | 3.75% |

| EUR | 2.15% |

| GBP | 3.75% |

| NZD | 2.25% |

| AUD | 3.85% |

| CAD | 2.25% |

| CHF | 0% |

| JPY | 0.75% |

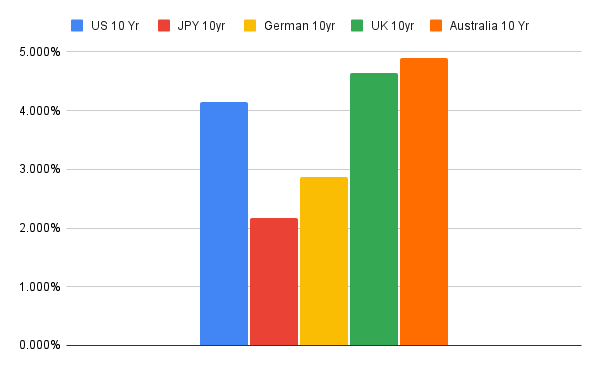

10-Year Government Bond Yields

| Country | 10-Year Yield |

|---|---|

| United States | 4.138% |

| Japan | 2.170% |

| Euro Area | 2.864% |

| United Kingdom | 4.641% |

| Australia | 4.888% |

Equity Markets vs Gold

| Index vs Gold | Ratio |

|---|---|

| S&P 500 | 1.30 |

| DAX | 5.30 |

| CAC 40 | 1.80 |

| FTSE 100 | 2.67 |

| Nikkei 225 | 0.068 |

Volatility

The VIX index sits near 29.49, a level that typically indicates elevated market stress.

While not at crisis levels, it signals that traders are preparing for large potential price swings.

Commodities

Gold–Oil Ratio: 56.79

This ratio provides insight into whether markets fear inflation, recession, or geopolitical disruption.

When both gold and oil rise together, it usually indicates:

- Inflation fears

- Supply shocks

- War risk

This aligns perfectly with the current macro environment.

Event Risk — What Could Move Markets

Even in a geopolitically driven environment, economic data can still trigger large currency moves.

The key event to watch this week is US unemployment claims.

US Initial Jobless Claims

- Previous reading: 213k

- Market expectation: 216k

Higher than expected claims:

Negative for the US Dollar as it suggests weakening labor conditions.

Lower than expected claims:

Positive for the Dollar because it signals continued economic resilience.