A concise summary of what matters most for FX this week: risk sentiment versus safe-haven flows, with gold as the compass.

Takezo Trading | 21/02/26

Reading time: 8 minutes

This Week’s Bottom Line

- Macro driver: Risk sentiment remains constructive, but gold’s strength is flashing early caution.

- Market regime: Risk-on — but not reckless.

- Key risks:

- Japan’s 10-year yields are rising. The carry trade is still alive, but if this accelerates, it can unwind violently.

- Gold is outperforming fiat currencies. That is classic safe-haven behavior — yet equities and volatility do not confirm a panic. I still classify the regime as risk-on.

- Gold remains elevated and consolidating as countries diversify reserves away from USD assets into bullion (notably China and Japan).

- Geopolitical risk: Escalation between the U.S. and Iran remains a tail risk capable of disrupting supply chains and sentiment.

Bias Map

- Pro-risk / anti-risk:

Pro-risk — supported by active Japanese carry trades and steady volatility.

Anti-risk triggers would include war spillover into Europe or broader U.S.–Iran disruption. - FX Watchlist:

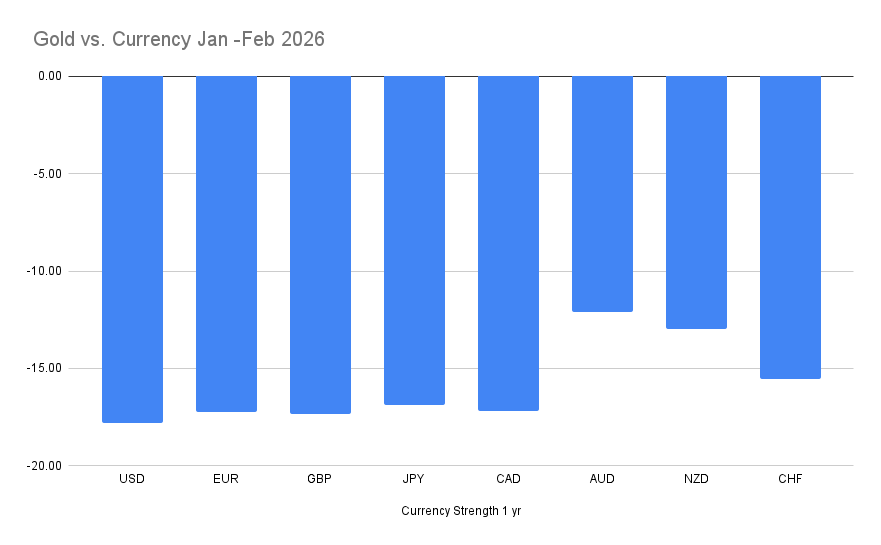

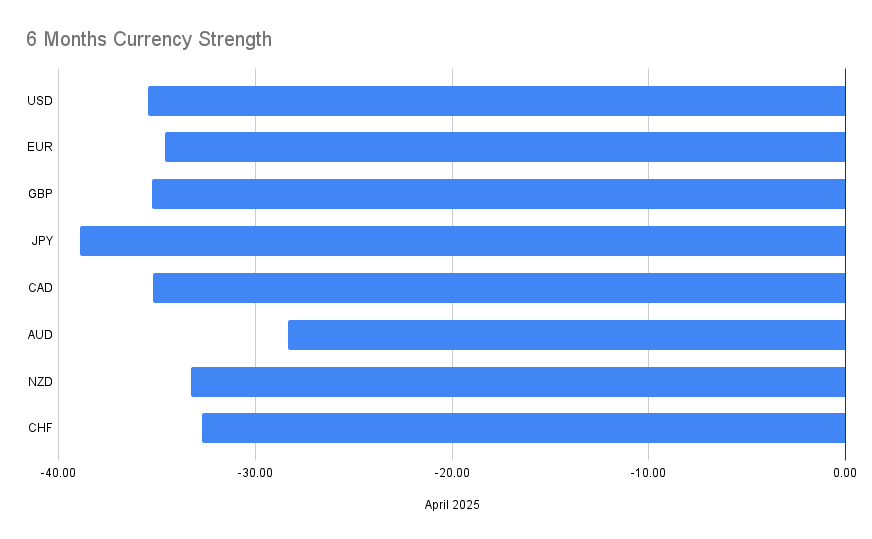

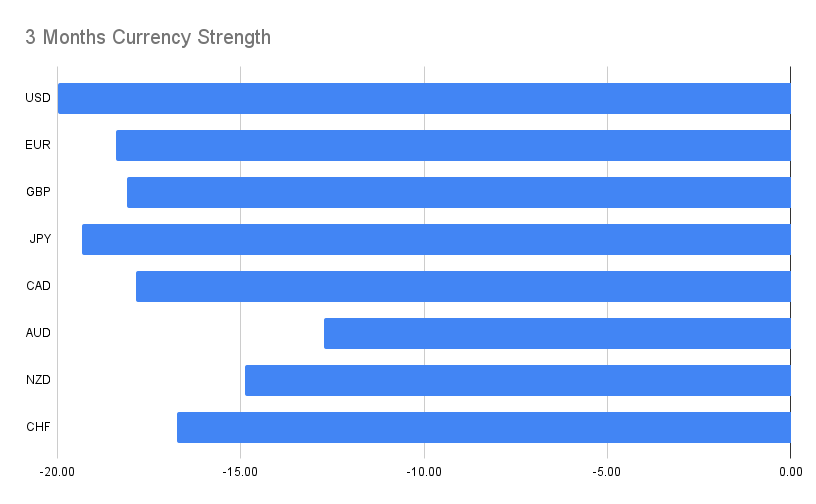

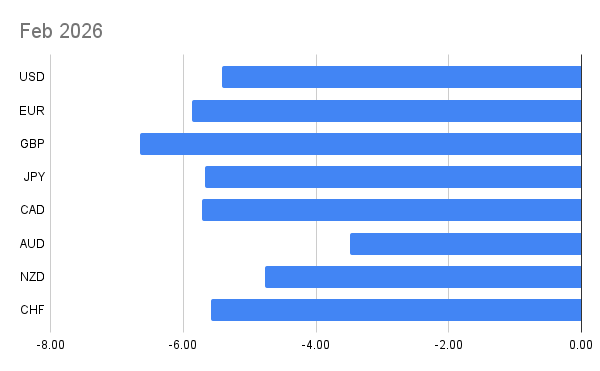

Focus on currencies versus Gold. Gold-relative strength remains the cleanest, most consistent signal across multiple timelines (February, 3-month, 6-month, and 2026 ).

Market Snapshot — What Happened Last Week

Rates

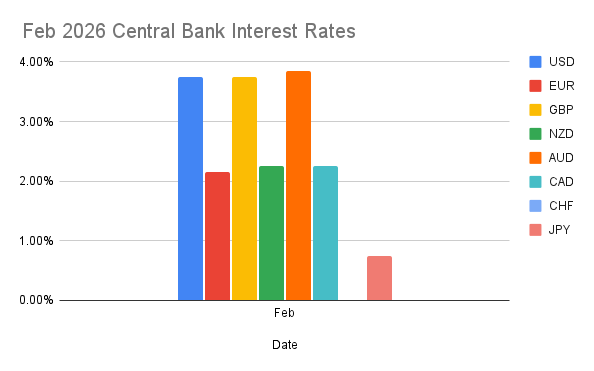

Central Bank Policy Rates

- USD: 3.75%

- EUR: 2.15%

- GBP: 3.75%

- NZD: 2.25%

- AUD: 3.85%

- CAD: 2.25%

- CHF: 0%

- JPY: 0.75%

The global rate structure still favors carry — particularly against low-yielders like CHF and JPY — but the margin of safety is narrowing as Japanese yields climb.

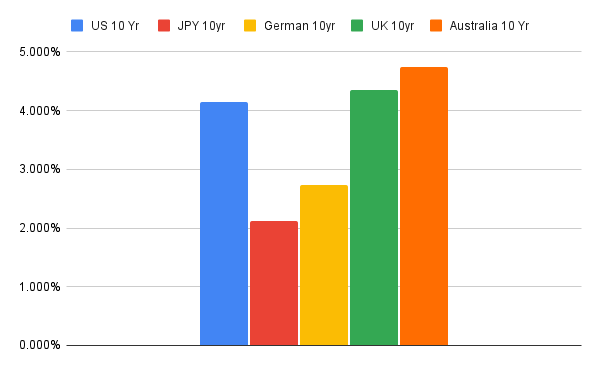

10-Year Government Bond Yields

- USD: 4.086%

- JPY: 2.115%

- EUR: 2.733%

- GBP: 4.352%

- AUD: 4.744%

The key development here is Japan’s 10-year yield at 2.115%. For years, the global carry system relied on suppressed Japanese yields. As that anchor lifts, the stability of leveraged positioning weakens.

Equities (Versus Gold)

- S&P 500 vs Gold: 1.35

- DAX vs Gold: 5.83

- CAC 40 vs Gold: 1.96

- FTSE 100 vs Gold: 2.82

- Nikkei 225 vs Gold: 0.072

Equities are not collapsing — but gold is not fading either. That divergence tells you capital is hedging without fully de-risking.

Volatility

- VIX: 19.09

Sub-20 VIX confirms that markets are not pricing systemic panic.

Commodities

- Gold/Oil Ratio: 77.01

For deeper context on this signal, review my full breakdown here:

https://takezotrading.com/the-gold-to-oil-ratio-a-historical-and-practical-guide/

A Gold/Oil ratio this elevated historically signals defensive positioning. The fact that equities and VIX are not aligned with that message is the tension defining this week.

Central Bank Scoreboard

Reserve Bank of New Zealand (RBNZ)

Headline Decision

- Hold: The Committee held the OCR at 2.25%.

- Decision style: Consensus hold.

No panic. No pivot. Just patience.

Inflation

Headline CPI remains temporarily above the target band due to specific components (food, electricity, council rates). Tradables volatility and administered prices are distorting the print.

Core inflation, however, is viewed as contained within the band, and the Committee expects headline inflation to moderate.

Implication:

They are not reacting emotionally to headline overshoots. Policy remains guided by underlying slack.

Growth / Labour Market

The economy is in an early-stage recovery.

The labor market is stabilizing, but unemployment remains elevated.

Households are cautious.

Implication:

Policy stays accommodative “for some time.” This caps NZD upside unless global risk accelerates.

Risk Assessment

Inflation risks are described as balanced:

- Downside: If household caution persists and recovery stalls, inflation may undershoot.

- Upside: If firms raise prices faster than expected during recovery, inflation could overshoot.

Balanced risks = no urgency to tighten.

Data Calendar & Event Risk

Tier 1 — What Can Change the Regime

USD Unemployment Claims

- Market pricing: 216k (previous: 206k)

If claims ≥ 216k:

Negative for USD (signals labor softening).

If claims < 216k:

Bullish USD (labor market resilience narrative intact).

This is important because rate expectations hinge heavily on labor resilience.

Commitment of Traders (COT)

For the latest breakdown of positioning extremes, see:

https://takezotrading.com/commitment-of-traders-update-feb-20th-2026/

Positioning tells you where pain trades are hiding.

Currency Strength vs Gold: Trades Appearing in Exactly 3 Timelines

AUDUSD – BUY

NZDUSD – BUY

USDCHF – SELL

EURGBP – BUY

EURJPY – BUY

EURCAD – SELL

GBPJPY – BUY

CADJPY – BUY

CHFJPY – BUY

NZDCHF – BUY

Currency Strength vs Gold: Trades Appearing in All 4 Timelines

EURAUD – SELL

EURNZD – SELL

EURCHF – SELL

GBPCAD – SELL

GBPAUD – SELL

GBPNZD – SELL

GBPCHF – SELL

AUDJPY – BUY

NZDJPY – BUY

AUDCAD – BUY

NZDCAD – BUY

AUDNZD – BUY

AUDCHF – BUY