A concise, macro‑driven view of what matters most for FX this week: carry dynamics, central‑bank divergence, and gold as a cross‑asset stress signal.

Takezo Trading | 31 January 2026

Estimated reading time: 6–8 minutes

This Week’s Bottom Line

- Primary macro driver: Central‑bank divergence remains the dominant force, with rate differentials still favoring risk‑aligned currencies while funding currencies lag.

- Market regime: Risk‑on, but cautious. Risk appetite persists, though it is increasingly selective and vulnerable to shocks.

- Key risks to monitor:

- Japan: Rising 10‑year JGB yields threaten the stability of the Japanese carry trade. If this move accelerates, carry unwinds could be abrupt.

- Gold vs fiat: Gold continues to outperform fiat currencies, signalling long‑term confidence erosion. However, other classic risk‑off indicators are not yet confirming a full regime shift.

- Geopolitics: Escalating tensions involving the US, Iran, and broader spillover risks into Europe remain latent tail risks for FX and commodities.

Bias Map (At‑a‑Glance)

- Risk stance: Net pro‑risk, with tight risk controls. Carry trades remain viable, but fragility is rising.

- FX focus: Pair selection guided by Gold vs Currency strength alignment across multiple timeframes.

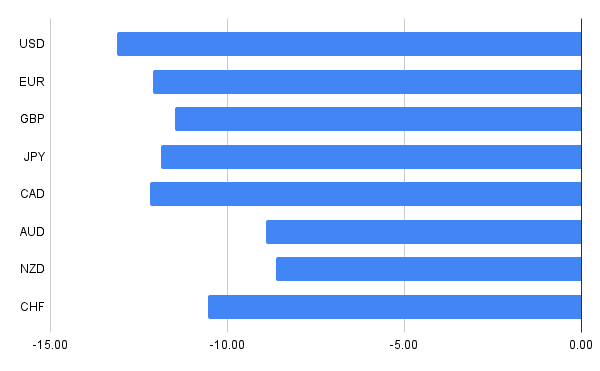

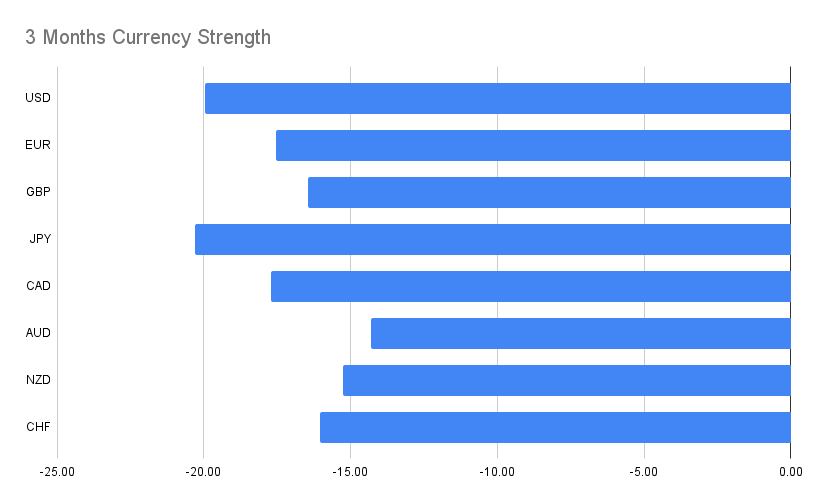

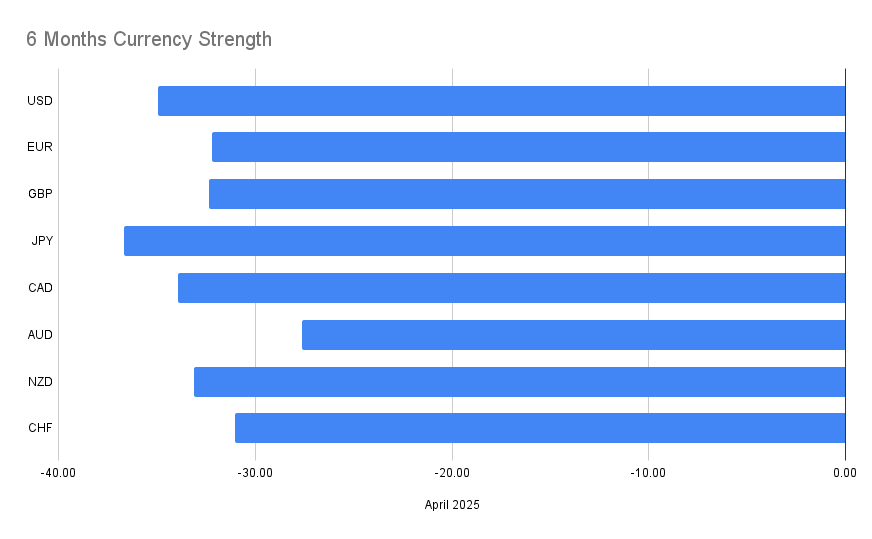

Cross‑Timeframe FX Alignment (Jan / 3‑Month / 6‑Month)

The following setups appear consistently across all three time horizons, with the same directional bias:

- EURUSD — BUY

- GBPUSD — BUY

- AUDUSD — BUY

- NZDUSD — BUY

- USDCAD — SELL

- USDCHF — SELL

- EURCAD — BUY

- EURAUD — SELL

- EURCHF — SELL

- GBPJPY — BUY

- GBPCAD — BUY

- GBPAUD — SELL

- AUDJPY — BUY

- AUDCAD — BUY

- AUDCHF — BUY

- NZDJPY — BUY

- NZDCAD — BUY

- CADCHF — SELL

Market Snapshot — What Happened Last Week

Interest‑Rate Landscape

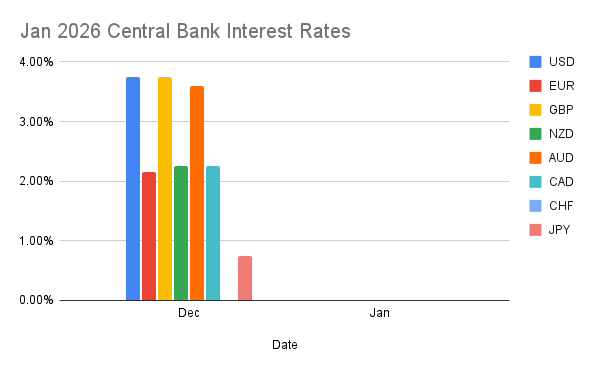

Policy Rates (Jan 2026)

- USD: 3.75%

- EUR: 2.15%

- GBP: 3.75%

- NZD: 2.25%

- AUD: 3.60%

- CAD: 2.25%

- CHF: 0.00%

- JPY: 0.75%

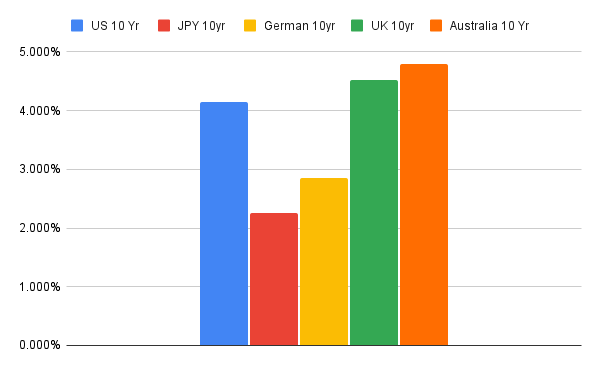

10‑Year Government Bond Yields

- United States: 4.239%

- Japan: 2.254%

- Euro Area (Germany): 2.847%

- United Kingdom: 4.525%

- Australia: 4.787%

The continued rise in longer‑dated yields — particularly in Japan — is a critical development. Yield compression has long underpinned carry strategies; any sustained reversal increases tail‑risk dramatically.

Equities vs Gold (Relative Stress Gauge)

- S&P 500 vs Gold: 1.42

- DAX vs Gold: 5.94

- CAC 40 vs Gold: 1.97

- FTSE 100 vs Gold: 2.86

- Nikkei 225 vs Gold: 0.07

Equities remain supported, but gold’s relative strength suggests hedging demand is rising beneath the surface.

Volatility

- VIX: 17.44

Volatility remains contained, reinforcing the current risk‑on bias — but levels are no longer complacent.

Commodities

- Gold‑to‑Oil Ratio: 74.44

Gold experienced a sharp sell‑off likely driven by profit‑taking, while oil spiked during the same period. Structurally, the ratio remains elevated, consistent with late‑cycle and geopolitical uncertainty dynamics.

For context please read my post here: https://takezotrading.com/the-gold-to-oil-ratio-a-historical-and-practical-guide/

Central Bank Scoreboard

Bank of Canada (BoC)

- Policy rate: Overnight rate held at 2.25%

- Vote: 8–1 majority

Interpretation: The BoC maintains a cautious hold. Inflation is projected near target, growth is modest, and trade‑related risks remain elevated. While there is subtle dovish optionality, the Bank stops short of signalling imminent rate cuts. CAD sensitivity remains skewed toward external shocks rather than domestic policy changes.

Federal Reserve (FOMC)

- Policy rate: Target range maintained at 3.75%

Hawk–Dove Scorecard:

- Inflation “somewhat elevated”: +1 hawkish

- Growth described as “solid”: +1 hawkish

- Labour market cooling: ‑1 dovish

- Policy action (hold): 0

- Elevated uncertainty / two‑sided risks: 0

- Two dissenters favoured a 25bp cut: ‑1 dovish

- Balance‑sheet operations supportive of liquidity: ‑1 dovish

Net score: ‑1 (slight dovish tilt)

Takeaway: The Fed is holding policy steady but internal pressure to ease is clearly building. Inflation remains the constraint, but the bias is slowly shifting toward eventual cuts.

Data Calendar & Event Risk — What Can Move Markets

Tier‑1 Events (High Impact)

- RBA Monetary Policy Statement — Mon, 2 Feb

Markets are pricing in a hawkish hold or hike. Any dovish surprise would likely weigh heavily on AUD. - BoE Monetary Policy Decision — Tue, 5 Feb

Expected to hold. A surprise hike would be GBP‑positive; unexpected dovishness would likely trigger downside volatility. - ECB Rate Decision — Tue, 5 Feb

Consensus expects no change. Hawkish language or a hike would support EUR, particularly against GBP. - US Initial Jobless Claims — Tue, 5 Feb

Forecast: 213k. A lower print would reinforce USD resilience and delay easing expectations.

It is a dense week for macro releases, increasing the probability of short‑term volatility spikes.

COT: For latest analysis of the commitment of traders data please go here: https://takezotrading.com/commitment-of-traders-update-jan-31st-2026/

Weekly Playbook — Actionable Wrap‑Up

- Primary driver: Yield differentials and carry‑trade stability.

- What flips the view: A sharp rise in JGB yields or a volatility breakout.

- Key risk days: RBA, BoE, ECB decisions; US labour data.

- Risk management: Keep size moderate and avoid over‑exposure ahead of major policy events.