The War Regime: Inflation Shock, Carry Trade Risk, and the Fragile Balance of Global Liquidity

By Takezo Trading | 04/04/2026

Reading Time: ~10–12 minutes

This week marks a critical inflection point in global macro. Markets are no longer reacting to isolated data prints—they are repricing an entirely new regime.

This Week’s Bottom Line

- Macro Driver: Geopolitical escalation (USA–Iran conflict) triggering an inflationary supply shock via oil

- Market Regime: Risk-on, but structurally unstable — liquidity remains, but cracks are forming

- Energy Shock: Closure of the Strait of Hormuz is a systemic event.

- Gold Behavior: Consolidation after an extended rally signals.

- Volatility: Elevated (VIX at 23.87) confirms uncertain positioning across risk assets

War is Inflationary

Markets often misprice war in its early stages.

Short-term: uncertainty → volatility

Medium-term: supply disruption → inflation

Long-term: policy tightening → economic stress

We are now transitioning from uncertainty phase → inflation phase.

The closure of the Strait of Hormuz is not just geopolitical theater—it is a global energy choke point. Roughly 20–30% of global oil flows through this corridor. Any disruption here cascades into:

- Higher transportation costs

- Rising production costs

- Sticky inflation globally

This is not theoretical. It is already being priced.

Understanding the Battlefield

Pro-Risk Forces

- Liquidity still present in markets

- Carry trades remain active (for now)

- Traders positioning for continuation of trends

However, this “risk-on” environment is fragile.

Anti-Risk Forces

- Elevated gold prices (safe haven demand persists)

- VIX at 23.87 — volatility is not low

- Expanding Middle East conflict involving major global players

This creates a dual-regime environment:

Markets are participating, but not confident.

The Japanese Carry Trade

This is where things get dangerous.

Japan is heavily dependent on imported energy. With oil supply disrupted:

- Energy costs surge

- Inflation rises domestically

- Pressure builds on the Bank of Japan to tighten

If BOJ raises rates:

→ The carry trade unwinds

→ Global liquidity contracts

→ Risk assets sell off

This is the silent trigger most traders are not fully pricing.

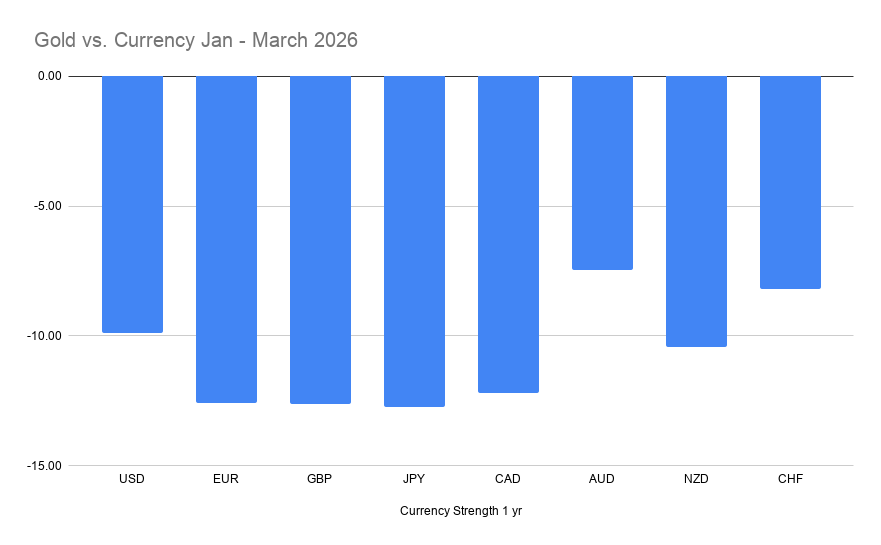

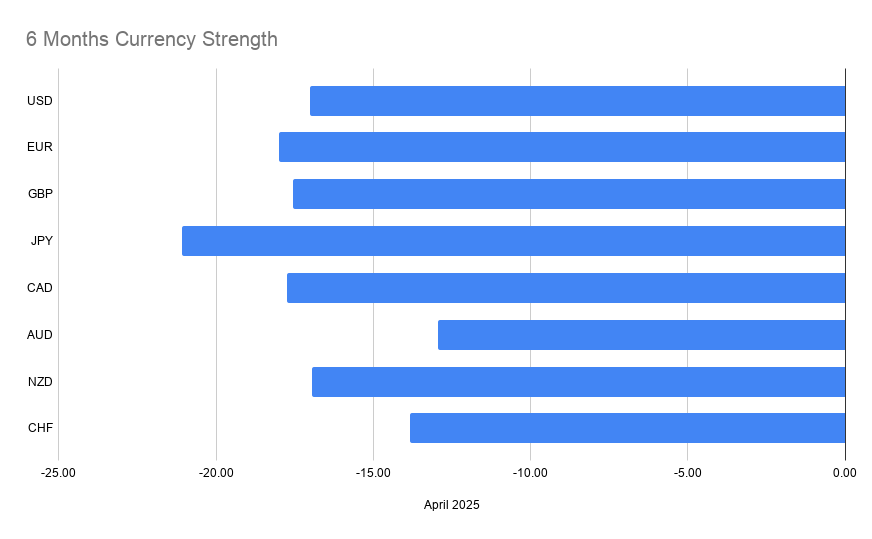

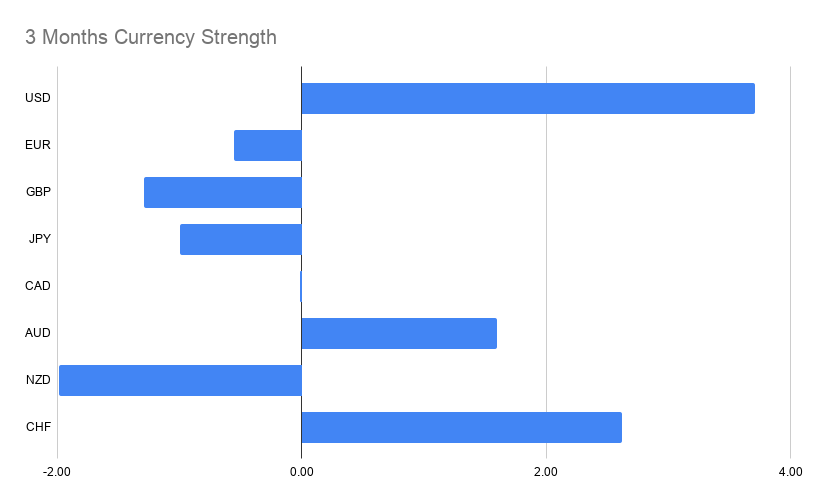

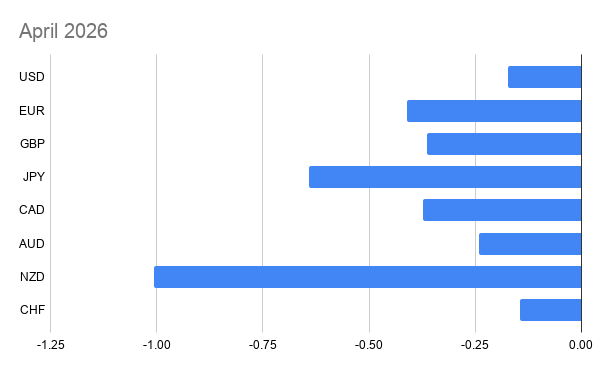

FX Watchlist — High-Conviction Setups

Trades Aligned Across ALL 4 Timeframes

- EURUSD – SELL

- GBPUSD – SELL

- USDJPY – BUY

- USDCAD – BUY

- NZDUSD – SELL

- EURJPY – BUY

- EURCAD – SELL

- EURAUD – SELL

- GBPAUD – SELL

- GBPCHF – SELL

- CADJPY – BUY

- AUDJPY – BUY

- CHFJPY – BUY

- AUDCAD – BUY

- CADCHF – SELL

- AUDNZD – BUY

- NZDCHF – SELL

Trades Aligned Across 3 Timeframes

- USDCHF – SELL

- EURCHF – SELL

- GBPJPY – BUY

- AUDCHF – BUY

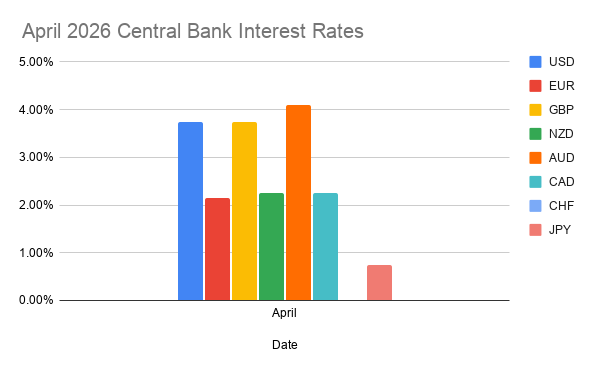

Interest Rates (Policy Landscape)

- USD: 3.75%

- EUR: 2.15%

- GBP: 3.75%

- AUD: 4.10%

- NZD: 2.25%

- CAD: 2.25%

- CHF: 0%

- JPY: 0.75%

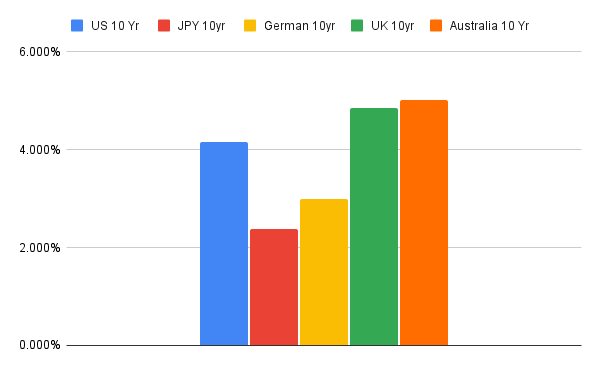

10-Year Bond Yields

- USD: 4.309%

- GBP: 4.851%

- AUD: 5.010%

- EUR: 2.996%

- JPY: 2.382%

Equities vs Gold (Risk Appetite Gauge)

- S&P 500 vs Gold: 1.41

- DAX vs Gold: 5.71

- Nikkei vs Gold: 0.071

Volatility

- VIX: 23.87

Commodities

- Gold/Oil Ratio: 41.77

Macro Deep Dive — The Inflation Chain Reaction

Here is the sequence currently unfolding:

- War disrupts oil supply

- Oil prices rise

- Inflation expectations increase

- Central banks forced into tighter policy

- Liquidity contracts

- Risk assets reprice

We are currently between steps 2 → 3.

Markets are not yet pricing steps 4–6.

That is where opportunity lies.

What Can Break the Market

Tier 1 Risks

- Escalation of USA–Iran conflict

- Further disruption in oil supply

- Central bank policy shifts (especially BOJ)

- Inflation data surprises

COT Positioning

For deeper positioning insight:

https://takezotrading.com/commitment-of-traders-update-april-4th-2026/